As part of a project helping a digital investment platform make its language easier to understand, we analysed the terms and conditions of the 13 largest UK banks offering current accounts, plus one challenger bank, for comparison.

“It would take 90 minutes to read the full terms and conditions of the average UK current account”

We specialise in financial services copywriting. That means we often do research into what the UK’s financial services providers are saying on their websites, apps and in other documents. We’ve been doing a lot of research into terms and conditions recently and thought it would be useful to share some of the findings.

Here’s what else we discovered:

All major UK banks have terms and conditions exceeding ten thousand words.

Nine have terms and conditions exceeding fifteen thousand words.

Four have terms and conditions exceeding twenty thousand words

One bank has terms and conditions exceeding THIRTY THOUSAND words.

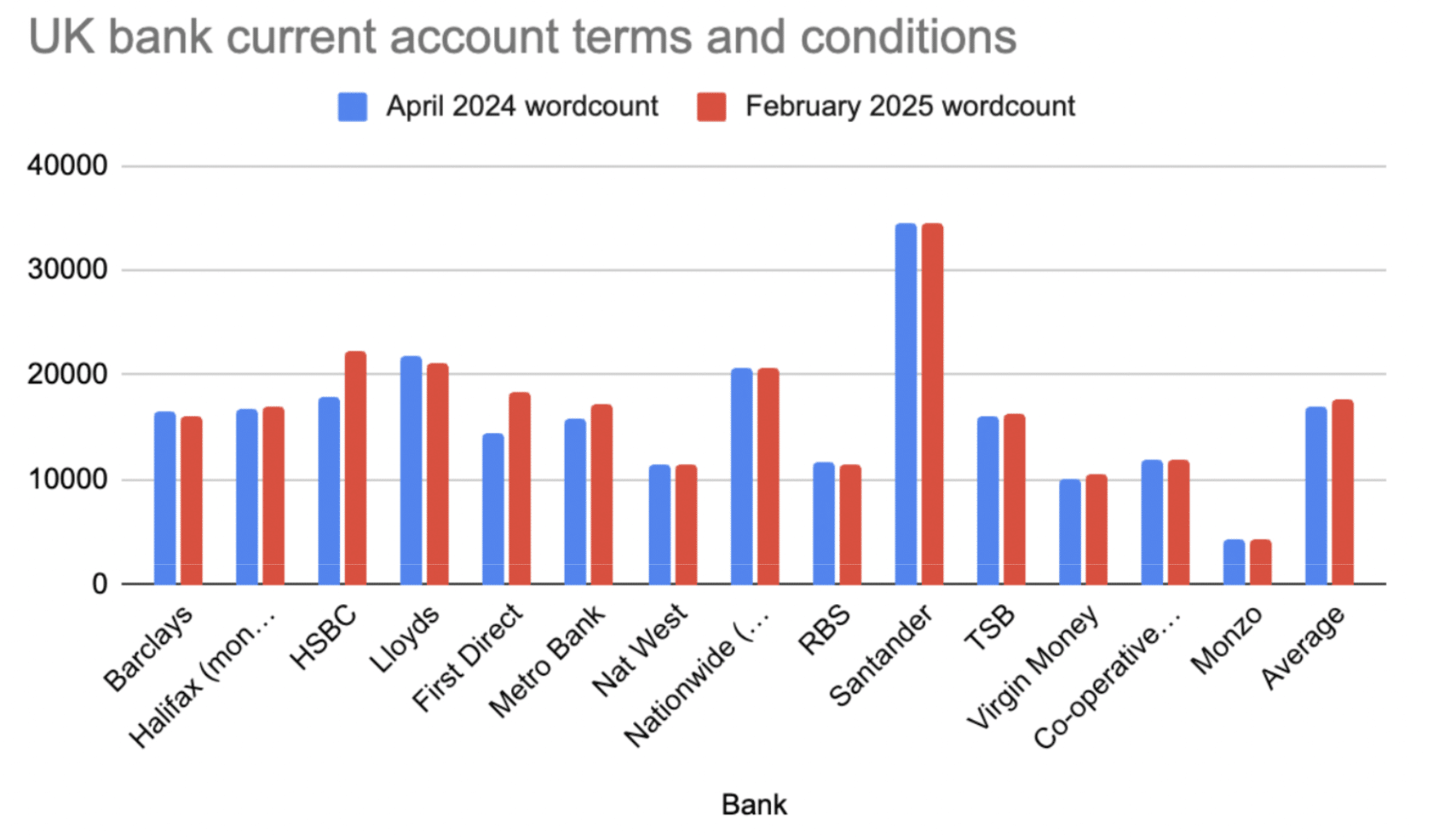

In August 2023, the average length of the leading banks’ terms and conditions was 16,771 words. By April 2024, that average had risen to 16,910, an increase of 0.8%. As of February 2025, the average length of a current account agreement is 17,614. That’s a 4% increase in length compared to last year and a 5% increase since 2023.

Our view as experts in financial services copywriting is that the vast majority of UK high street banks have terms and conditions that are inaccessible purely due to their length.

There are other factors that make these terms and conditions inaccessible too, like complex language and jargon, but the length of these documents necessarily makes them inaccessible.

“You could read all of John Steinbeck’s Of Mice And Men faster than you could read this bank’s current account terms and conditions”

| Bank |

Terms and conditions word count

|

| Santander | 34,519 |

| HSBC | 22,221 |

| Lloyds | 21,206 |

| Nationwide (Flex Plus) | 20,762 |

| First Direct | 18,399 |

| Metro Bank | 17,158 |

| Halifax (moneysmart) | 16,887 |

| TSB | 16,408 |

| Barclays | 16,168 |

| Co-operative Bank | 11,941 |

| RBS | 11,456 |

| Nat West | 11,438 |

| Virgin Money | 10,429 |

| Monzo | 4192 |

Let’s put these documents into context.

When the German High Command surrendered at the end of World War II, the document they signed to make it official was 234 words long.

When the United States declared independence from the British on July 4th 1776, the document they signed was 1,320 words long. That’s about 3% the size of Santander’s current account terms and conditions.

The average reading time required to read the terms and conditions of a UK high street current account is 90 minutes. That’s as long as a professional football match.

Assuming an average reading speed of 200 words per minute, you could finish reading John Steinbeck’s Of Mice And Men before you finished reading Santander’s current account terms and conditions.

Don’t terms and conditions need to be long though, by definition?

No.

It might be intuitive to assume, being complex things (terms and conditions should not that complex), that we need long and hard-to-digest terms and conditions.

This simply isn’t the case. And we have an example to prove it.

Not included in our round up above, due to their size, was Monzo, the app-based bank. Their current account terms and conditions, as of February 2025, are 4192 words long. It would take about 19 minutes for someone with average reading comprehension to finish reading them

So why are terms and conditions so long?

A quote commonly attributed to Mark Twain goes something like this: “I didn’t have time to write you a short letter, so I wrote you a long one.”

Brevity takes effort. It’s hard to communicate in simple terms and keep it to the point. The other challenge, which we’ve addressed in a separate post, is what the bank regulator calls over disclosure. Over disclosure is when service providers, in this case banks, declare and disclose every feasible version of a scenario in order to protect themselves from litigation.

We can see it happening in real time, albeit slowly, with the above sample. The terms and conditions are growing slowly because banks keep adding new clauses and exclusions.

The Financial Conduct Authority has been warning against this practice since 2016, when it identified a persistent problem with banks including far too much information in their terms and conditions.

“One fundamental barrier to improving T&Cs is the over-disclosure approach adopted by firms as a mechanism to mitigate perceived risk of litigation. In our view, we consider this concern should not prevent firms doing more to improve the quality and effectiveness of T&Cs.” – FCA guidance note.

Banks appear to be scared of simplifying their terms and conditions for fear of inviting litigation. They needn’t be. Mozno, and also the client we worked with who inspired this research, have proven that it’s possible to publish compliant, useful terms and conditions without forcing customers to sift through tens of thousands of words.